The global economic situation has become increasingly challenging. A fragile, interconnected economy has been hit by repeated shocks. The fragmentation within and between countries, industries and governments has meant these shocks have manifested into a shared environment where competition for resources is fierce. This has led to inflationary pressures crossing national boundaries and impacting living standards. The UK continues to face steep challenges, shaped by the lingering effects of a trilogy of successive events: Brexit, Covid-19 and the war in Ukraine. Each has, to varying degrees, reinforced geopolitical risk, economic uncertainty and supply disruptions, contributing to weakened business activity and falling household incomes.

Bharthi Keshwara, CMI’s economist

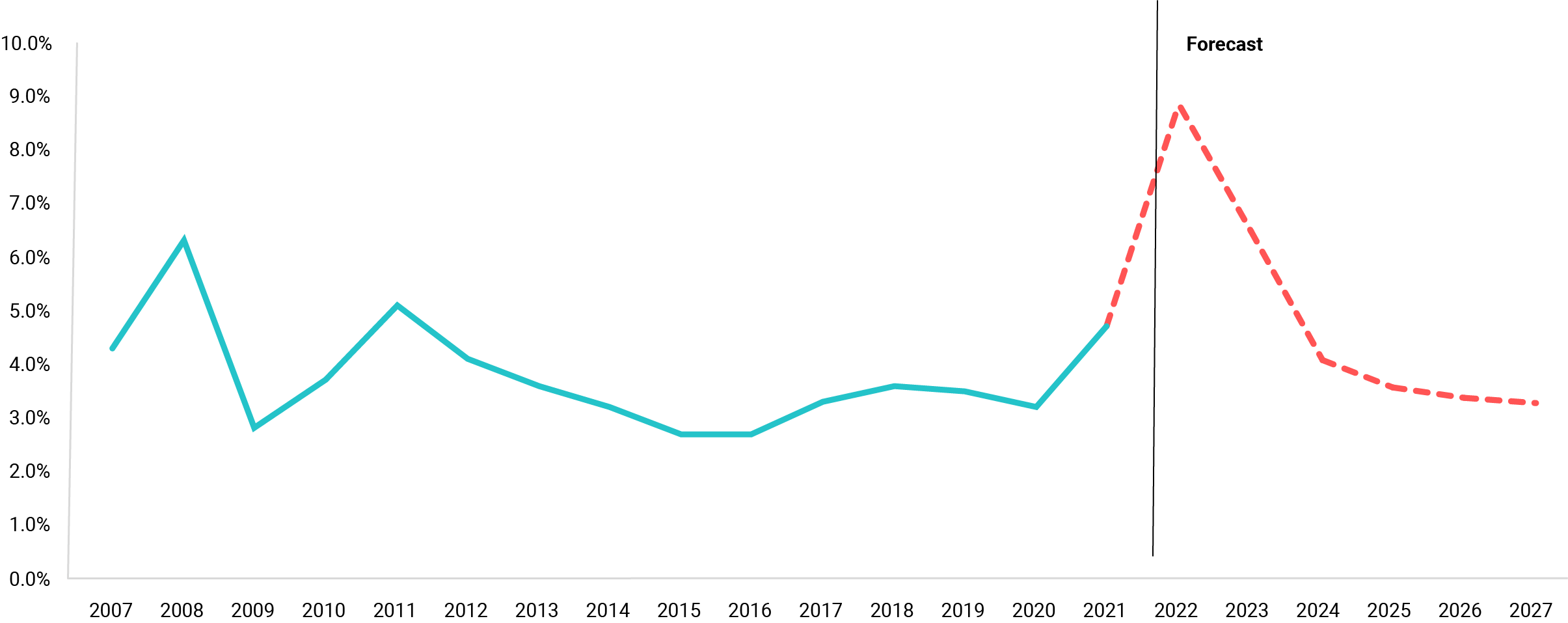

According to the International Monetary Fund (IMF), global economic growth is forecast to nearly halve from 6% in 2021 to 3.2% in 2022. This is the weakest growth expectation since 2001, aside from the 2008 global financial crisis and the Covid-19 pandemic. This translates into slowdowns in all of the world’s large economies. Indeed many economists believe that the UK economy will enter a recession in 2023, echoed by official growth figures that have confirmed the first contractionary quarter(Fig.1). Interestingly, a recent CMI Managers Voice survey reinforced this view when it found eight out of every ten managers felt that the UK was already in a recession – signalling a mounting mood of pessimism that may settle in.

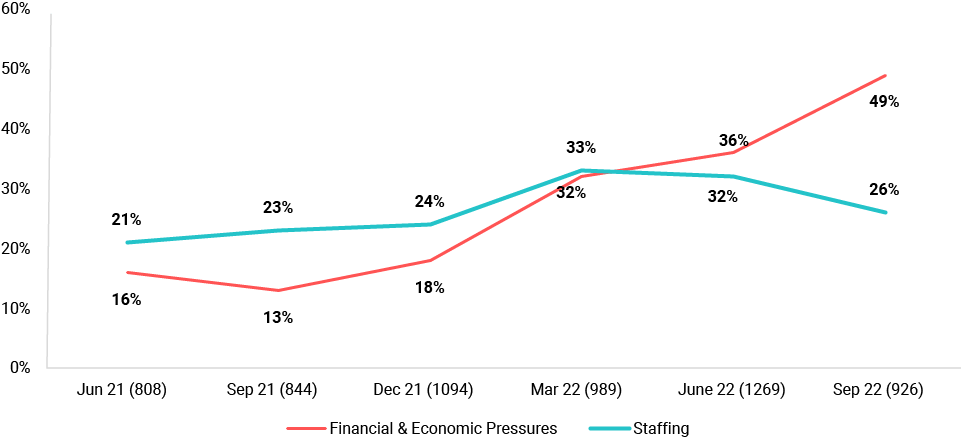

Managers and leaders have to remain equipped and resilient throughout periods of turbulence, but remaining steadfast is never easy. Our latest CMI Managers Concerns survey found that respondents are primarily concerned about financial and economic pressures, followed by staffing concerns (Fig.2). And although staffing concerns remain at a high level, they have continued to slow over the last quarter in line with falling job vacancies, indicating that financial pressures are likely to force businesses to rein in hiring activity – indeed they may be already, given that business insolvencies are at their highest level in over a decade.

In addition to the current macroeconomic headwinds, the fragile global economy is also in transition from a tangible to an increasingly intangible economy – an economy that has organisations with a majority of investment in knowledge assets such as design, training and business processes. These assets are embedded in its human capital, organisational processes and digital software rather than tangible bricks-and-mortar and machinery. As Jonathan Haskel, Bank of England MPC member, and Stian Westlake, CEO of The Royal Statistical Society, wrote in Capitalism without Capital, in this environment it becomes more important that during outbursts of macroeconomic volatility, managers are able to reduce the risk of losing intangible assets and investments, especially in knowledge-intensive firms.

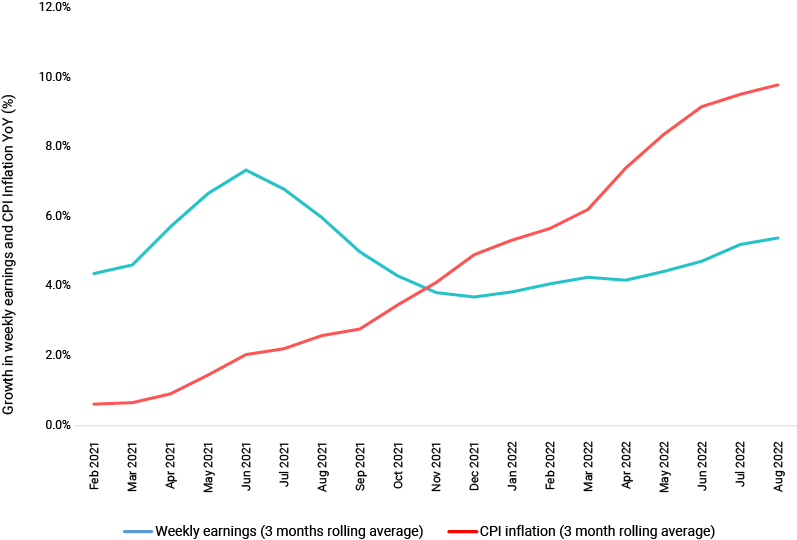

So in the face of weakening demand, labour shortages and increasing costs such as meeting requests for higher pay as wages lag behind inflation (Fig.3), and interest rate hikes that translate into higher borrowing costs (Fig 4), managers need to be innovative and creative to strengthen the supply side of their business.

As the UK moves into a period of recession and austerity, it’s really important that we train our managers and leaders for the challenges that lie ahead… what’s actually needed first is innovation – they need to look first for smart workarounds and find innovative ways of solving problems and delivering products and services… Many of today’s managers and leaders won’t have lived through a recession before and we can’t afford for them to make the same mistakes as previous generations

Mike Durke CMgr FCMI, Swansea councillor and senior lecturer, University of Wales Trinity St David

A recent CMI survey revealed only slightly more than half of the UK’s managers feel their organisation's leaders have the skills to lead through an economic downturn and just under half of the managers felt they had sufficient training to support their organisation and employees in difficult situations. There are three key steps within CMI’s Professional Standards that may help and support managers and leaders through this volatile time.

1. Acquire knowledge

In a period of heightened uncertainty and tightening financial conditions, decision-making becomes more complex. Information, about areas such as economic context, markets, users or consumers, and your organisational capacity, becomes an increasingly valuable commodity. It enables one to limit uncertainty and make sure that decisions and judgments are evidence-based, credible and trustworthy. CMI will continue to produce quarterly economic outlook reports tailored to managers and leaders in order to help inform the context of some of these insights.

2. Harness communication

As uncertainty and volatility among the workforce and suppliers increases due to external factors, it is important to share new information across your organisation and surface ideas and experience, as you consider the best response. Transparency and communication may also help you retain talent in a competitive labour market.

Second, it’s vital to co-ordinate with key stakeholders in your supply chains. This could help shield you from the most acute cost and competitive pressures and minimise surprises from supply chain disruption.

3. Develop people

Financial and revenue growth is the aim of many managers and leaders. But in order to grow, an organisation’s resources (supply side) also need to be built up. Otherwise true growth and productivity will remain elusive. In the current tight labour market, where there are more vacancies than people looking for a job, labour supply is one of the key challenges for many managers.

To tackle the issue, managers and leaders must develop existing talent to improve productivity and strengthen the supply side. One way of doing this is training and upskilling talent. Recent CMI modelling on apprenticeships has found that at a national-level initial training investment in apprenticeships of £2bn could return c.£7bn over a decade to UK employers and the economy. Not only does investment in the human capital of an organisation lead to greater output, it also keeps talent engaged in the workplace community, boosts morale and helps retain talent. Training can also help organisations evolve to become fit for the future. For example, taking steps today to train staff on working towards achieving net-zero targets will not only provide long-term cost savings, but will protect businesses from future energy price spikes.

As competition for resources intensifies, shortages are arising, and cost pressures are mounting. At such times of crisis when materials and finance are in short supply (Fig 5), managers and leaders need to maximise resources that remain plentiful: coordination, communication and compassion. We face shared challenges so let’s look at how we can work collectively to coordinate solutions across borders - for example through industry networks and pan-national policy solutions. By focusing on a common good of stability, managers and leaders may be able to reduce the extent and duration of the stresses that businesses and households are currently facing.

The management ripples: a volatile global economy in five charts

Here we unpack some of Bharthi's key data insights.

Costs are rising: outturn & growth forecast consumer prices, annual (yoy%)

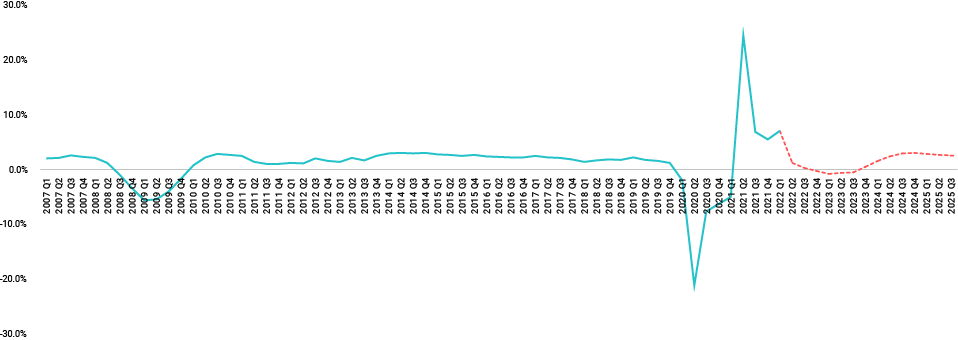

The future looks flat: outturn & growth forecast GDP growth, quarterly (yoy%)

Financial pressures are paramount: Managers' key concerns as a share of their total concerns

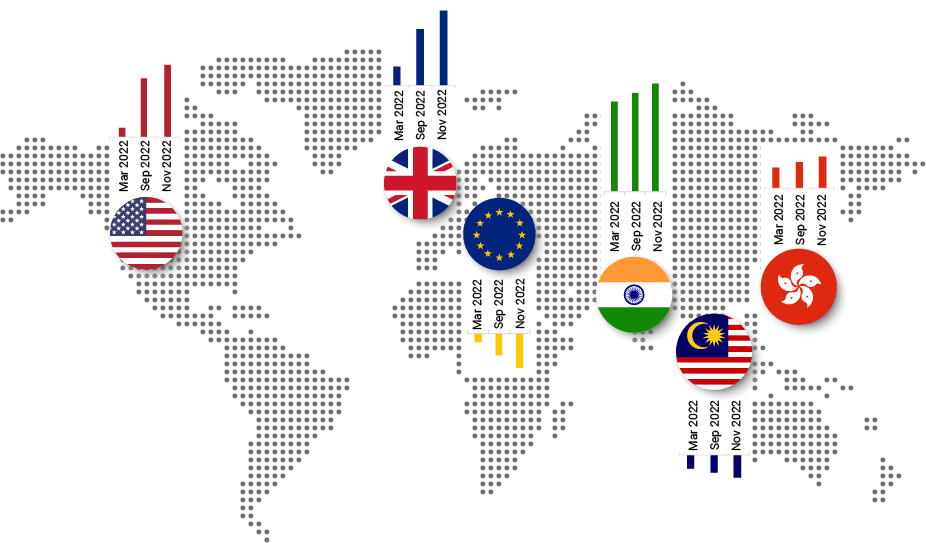

Global credit costs soar: growth in bank rates across the world

How far wages stretch: growth in weekly UK earnings and CPI inflation (yoy%)

More from CMI

- Managers Voice is an exclusive Community of CMI managers representing the voice of UK management. Here’s how to get involved

- Expand your capacity for resilience with CMI’s Building resilience skills refresher course

- Communicating under presser skills refresher

- Watch this digital event: Decision Making in Uncertain Times